Backtesting Options Selling Strategies: The Key to Profitable Automation SEO Meta

Don't trade on a guess. Understand why backtesting is the most critical step in options automation and what key metrics you need to evaluate for profitable, data-driven strategies.

Backtesting Your Options Strategy: The Key to Profitable Automation

In the world of automated trading, a strategy is merely a hypothesis until it has been rigorously tested. The process of validating a trading idea against historical market data is known as backtesting, and it is the single most important step before deploying any capital. For options traders, especially those employing automated selling strategies, effective backtesting is the foundation of long-term profitability.

Why Does Backtesting Matter for Options Selling Strategies?

Backtesting allows you to answer the fundamental question: Has this strategy worked in the past, and under what conditions? It provides a quantitative measure of a strategy's potential performance, resilience, and risk profile. Without it, you are simply guessing.

The challenge with options is the complexity of the data. Options prices are influenced by five main factors (the "Greeks"), and simulating their behavior over years of market history requires massive computational power and clean, high-quality data. This is why an automated platform is essential for backtesting options selling strategies.

What are the Risks of Not Backtesting?

•Curve Fitting: A strategy that looks good on paper might only work for a very specific, short period of time. Backtesting across diverse market conditions exposes this flaw.

•Unforeseen Drawdowns: Without testing, you have no idea what the maximum historical loss (Max Drawdown) of your strategy is, leading to panic and premature strategy abandonment during inevitable losing periods.

•Ignoring Transaction Costs: Manual testing often overlooks the impact of commissions and slippage, which can turn a profitable strategy into a losing one when deployed live.

How Does an Automated Platform Transform Backtesting?

While you could attempt manual backtesting with spreadsheets, the process is time-consuming, prone to error, and often lacks the granularity of real-world execution. An automated platform transforms this process by offering speed and accuracy:

Access to Clean, Comprehensive Historical Data

A professional options trading platform features access to years of clean, tick-by-tick options data. This is crucial because a small error in historical pricing can drastically skew the results of a backtest. The platform handles the data sourcing and cleaning, allowing you to focus on the strategy.

•High-Fidelity Data: The platform uses data that accounts for corporate actions, dividends, and other events that impact options pricing, ensuring your simulation is as close to reality as possible.

•Data Normalization: It normalizes the data, making it easy to test a strategy on different underlying assets without worrying about data format inconsistencies.

Simulating Real-World Trading Conditions

A good backtesting engine doesn't just look at closing prices; it simulates the actual conditions of the trade, including:

•Slippage and Commissions: The engine allows you to input your actual broker's commission structure and a realistic slippage estimate, providing a true net profit figure.

•Early Assignment Risk: It simulates the possibility of early assignment on short options, especially around ex-dividend dates, a critical risk for options sellers.

•Market Volatility: The platform allows you to test the strategy's performance during periods of high and low volatility, ensuring the strategy is robust across different market regimes.

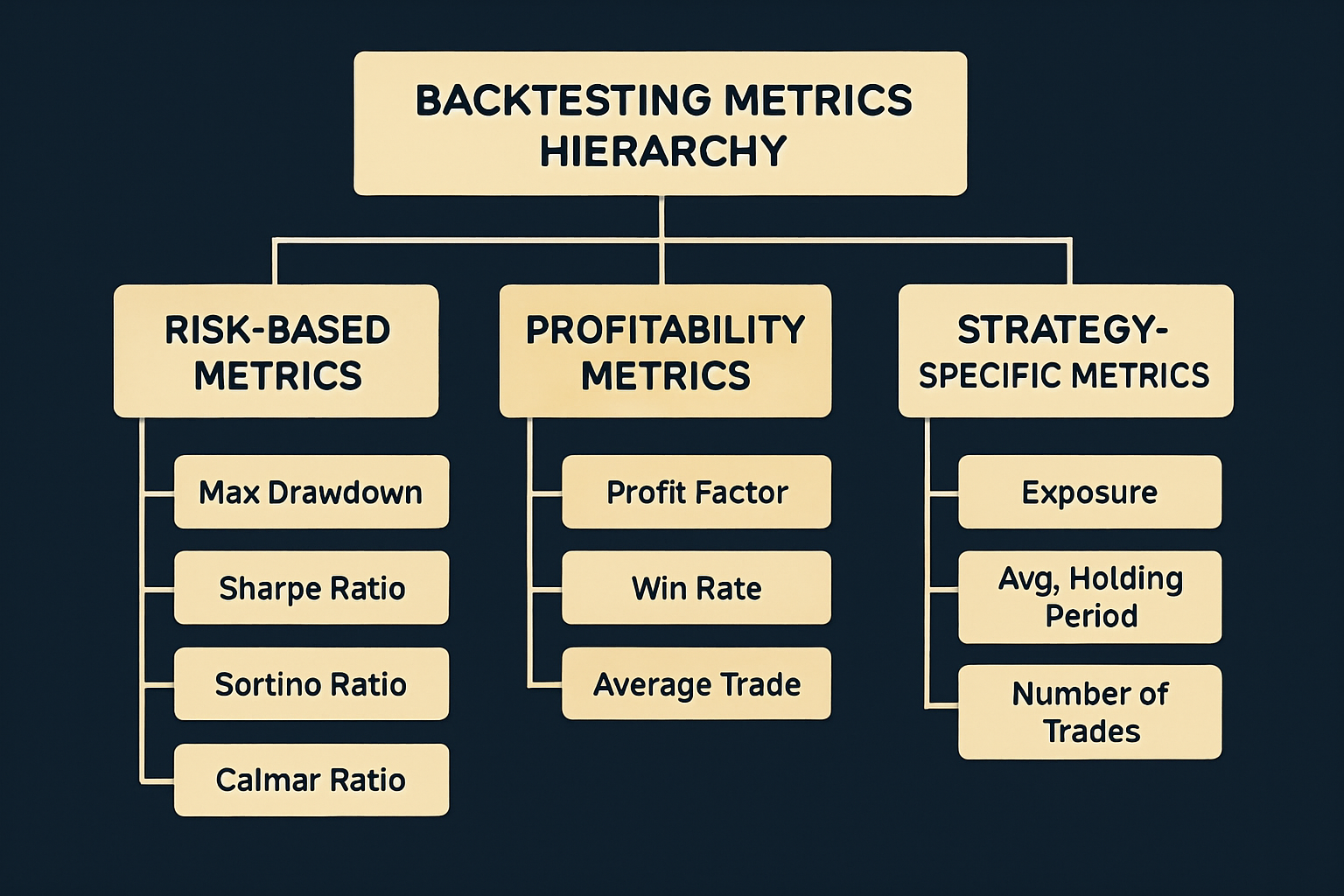

What Key Metrics Should You Evaluate in Your Backtest?\n\n### Visual Guide: Backtesting Metrics Hierarchy\n\n

A backtest provides a wealth of data, but a few key metrics are non-negotiable for evaluating strategy performance:

1. Risk-Based Metrics (The Most Important)

•Max Drawdown: This is the largest peak-to-trough decline during a specific period. It measures the worst-case scenario, and a low drawdown is critical for capital preservation. If your strategy has a 30% Max Drawdown, you must be prepared to lose 30% of your capital before the strategy recovers.

•Sharpe Ratio: This measures the risk-adjusted return. It tells you how much return you are getting for the level of risk you are taking. The higher the ratio, the better the return for the level of risk taken.

•Sortino Ratio: Similar to the Sharpe Ratio, but it only considers downside volatility (bad volatility). This is often preferred by options sellers who are primarily concerned with capital loss.

2. Profitability Metrics

•Profit Factor: This is calculated by dividing Gross Profits by Gross Losses. It is a measure of the strategy's efficiency. A factor above 1.5 is generally considered good, meaning you make $1.50 for every $1.00 you lose.

•Annualized Return: The average return the strategy would have generated over a year. This allows for easy comparison with benchmarks like the S&P 500.

•Win Rate: The percentage of trades that closed profitably. Options selling typically has a high win rate (often 70%+), but this must be balanced with the Risk/Reward ratio.

3. Strategy-Specific Metrics

•Average Days in Trade: How long the bot holds a position. This is crucial for options selling, as you want to capture Theta decay efficiently.

•Exposure Metrics: Metrics that track the average Delta, Gamma, and Vega exposure of the portfolio over the backtest period. This helps you understand the strategy's sensitivity to market direction, acceleration, and volatility.

How Do You Transition From Backtest to Live Bot?

The final advantage of using an integrated platform is the seamless transition from a validated backtest to a live trading bot.

•One-Click Deployment: Once your backtesting options selling strategies are complete and the results are satisfactory, you can deploy the exact same logic with a single click. This eliminates the risk of coding errors or misinterpretation between the testing and live environments.

•Paper Trading Bridge: The best practice is to first deploy the strategy to a paper trading account for a few weeks. This "forward testing" ensures the bot's logic interacts correctly with the live market data feed and your broker's API before any real capital is at risk.

•Continuous Monitoring: Even after going live, the backtest results serve as a benchmark. If the live bot's performance deviates significantly from the backtest (e.g., a much higher drawdown), it signals that the market regime has changed, and the strategy needs to be re-evaluated.

Conclusion: Validate Your Edge\n\n

In automated options trading, your edge is your validated strategy. Backtesting is the process of validation, turning a hopeful idea into a statistically proven system. Do not trade a strategy that has not been rigorously tested.

Use OptionBots' powerful backtesting engine to validate your next winning strategy and ensure your automated trading is built on a foundation of data, not speculation. The time invested in thorough backtesting is the best insurance policy for your trading capital.